Analysts are divided on the impact of Open USD, a new competitor stablecoin introduced by Stripe and others, which has caused investor concern.

- Circle Internet Group's stock fell over 17% on Tuesday and was trading in the green in pre-market trading on Wednesday.

- Compass Point upgraded Circle’s rating from 'Sell' to 'Neutral', lowering the price target from $97 to $55, a downside of 11.3%.

- A William Blair analyst maintained an 'Outperform' rating with a $650 price target, arguing that the market reacted excessively to competition fears.

- The launch of Open USD involves major companies such as Visa, Mastercard, and Coinbase, raising concerns about Circle's distribution and revenue models.

Shares of Circle Internet Group (CRCL) rebounded in early Wednesday trading after suffering their biggest post-IPO decline a day earlier, but the recovery has done little to settle one question on Wall Street: Is the launch of rival stablecoin Open USD a serious threat to Circle's business or an overblown concern?

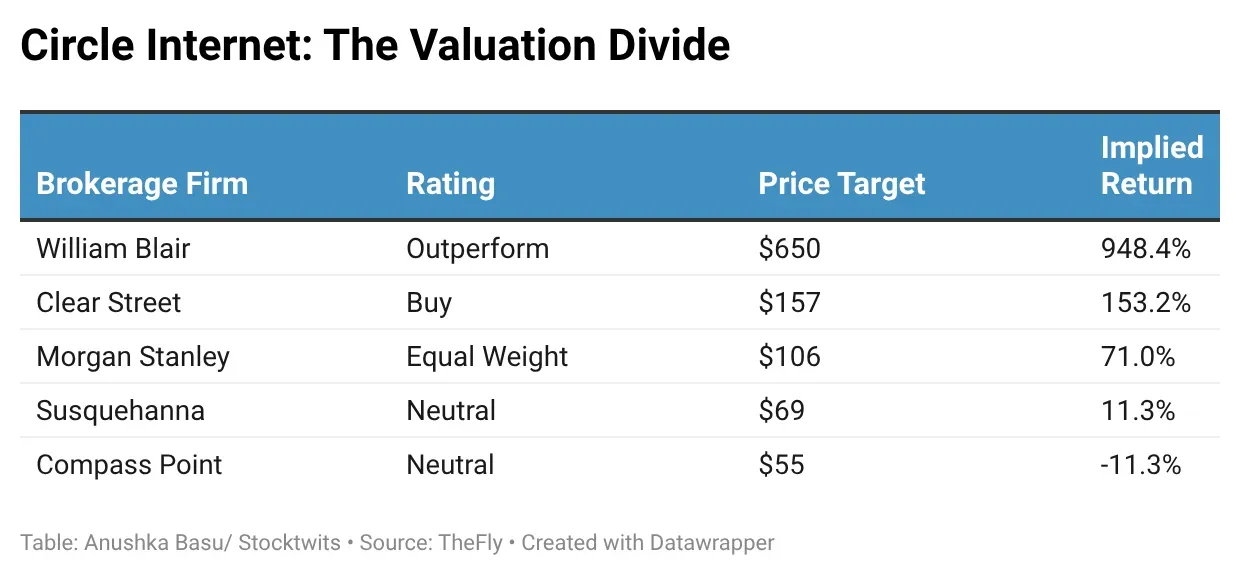

Analyst price targets now range from as low as $55 to as high as $650, highlighting an unusually wide divide over Circle's competitive position, valuation and long-term role in the fast-growing stablecoin market.

Why OpenUSD Spooked CRCL Investors On Tuesday

A number of major payment, banking, and crypto companies, including Visa (V), Mastercard (MA), Stripe, BlackRock (BLK), and Coinbase (COIN), are supporting a new dollar-backed stablecoin called Open USD (OUSD).

As part of the new system, coalition members would retain revenue from reserve assets, while Circle paid Coinbase almost $908 million in 2024 for distributing USDC. This has raised questions about Circle’s distribution model and revenue model, with interest on USDC reserves accounting for more than 99% of its income.

CRCL stock was trading at $63, up over 2% in pre-market. On Stocktwits, Circle's stock was one of the top-trending tickers.

Wall Street Splits On The Threat: The Bears

Compass Point raised Circle to 'Neutral' from 'Sell' but lowered its price target to $55 from $97 - a value call after the selloff. The company saw the Open USD debut as a negative development for Circle's long-term prospects in payments, citing OUSD's ties to large payments businesses and its network, which includes Circle's own asset management partners, according to TheFly.

Compass Point said it does not see Open USD gaining traction in DeFi or crypto trading, which are the core use cases for USD Coin (USDC), and does not see the launch meaningfully impacting Circle’s Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) over the next two years. The brokerage also noted the planned Aug. 18 renewal of Circle’s USDC collaboration with Coinbase (COIN), which it said might relieve the overhang on the stock.

Susquehanna analyst James Friedman initiated coverage of Circle with a ‘Neutral’ rating and $69 price target, implying some 11% upside from Tuesday’s close. The analyst said Circle is a first mover in a strategic market and is "building one of the most important franchises in digital finance," and has the potential to become the "Globe's Digital Dollar." However, he warned that Circle remains almost entirely dependent on reserve income, that its economics are not unique, and that the valuation “looks full,” even if outcomes may “differ widely.”

Some Analysts See Upside For Circle

William Blair analyst Andrew Jeffrey didn’t see it that way. Jeffrey kept an ‘Outperform’ rating with a $650 price target on the stock, arguing that it overreacts to competitive fears and that investors should buy it, according to reports. Competition in the $20-plus trillion stablecoin market is inevitable and further validates the commercial opportunity for Circle and USDC, Jeffrey added.

The selloff in Circle Internet’s shares yesterday was “excessive”, said Owen Lau, an analyst at Clear Street. Open USD has good partners like other top stablecoins, but there is no hard evidence it can gain real traction, and the sell-off in Circle looks overdone, the analyst told investors in a research note.

“While the narrative will linger, CRCL has maintained strong market shares even though new stablecoins continuously arise," the firm argued. It maintained a 'Buy' rating and set a $157 price target on Circle Internet.

Morgan Stanley said it is "very unlikely" Coinbase will walk away from its Circle partnership at the August renewal, as the deal remains favorable to it. The analyst said that Coinbase’s position in the rival consortium “could be raising the temperature” without necessarily complicating the renewal. Morgan Stanley has a $106 price target and an ‘Equal Weight’ rating on Circle.

The Valuation Divide

But Retail Keeps Buying The Dip

Despite the debate on Wall Street, retail traders appear to view Tuesday’s selloff as a buying opportunity. Retail sentiment around CRCL improved to ‘extremely bullish’ from the ‘bearish’ zone over the past day. Chatter around it improved to ‘extremely high’ from ‘high’ over the past day.

One Stocktwits user said the recent sell-off in Circle is driven more by fear than by facts. Many on the platform remained bullish, saying that a list of partners backing a project does not automatically mean a real-world use case.

Circle’s stock was down over 21% so far this year.

Read also: Trump's Disclosed Crypto Holdings Sink Nearly 40% In Value Since Disclosure Date

For updates and corrections, email newsroom[at]stocktwits[dot]com.<