The CEO said he will not replicate the perpetual preferred structure at his own Bitcoin treasury company.

- Twenty One Capital CEO Jack Mallers said companies issuing perpetual preferred equity are "signing up to owe money forever".

- The comment expanded his BTC Prague critique of Strategy (MSTR) Executive Chairman Michael Saylor in a follow-up podcast.

- Mallers contrasted the new model with older convertibles that could be retired through equity conversion at a premium.

Twenty One Capital CEO Jack Mallers said companies issuing perpetual preferred equity are "signing up to owe money forever," expanding his BTC Prague critique of Strategy (MSTR) Executive Chairman Michael Saylor in a follow-up podcast appearance.

The comment targeted a structural feature of the newer instruments that Strategy has used to raise capital, including its preferred stock called Variable Rate Series A Perpetual Stretch Preferred Stock commonly known as Stretch (STRC). Unlike convertible bonds, the perpetual preferreds are non-callable, do not convert into equity, and carry a coupon of about 11.5% forever, Mallers said in an interview with the BTC Prague team.

The concept was different from the prior MicroStrategy convertibles raised in the post-COVID era, with coupons as low as 0% and which could be retired by converting to equity at a premium, Mallers said. That approach allowed the corporation to effectively wipe the instruments off its capital structure. The new perpetuals can never be wiped out, Mallers said.

Twenty One Capital (XXI) CEO outlined the four options facing any Bitcoin treasury business with an underwater Bitcoin position and common shares that it cannot issue accretively. The business might sell Bitcoin, issue dilutive common, discontinue paying preferred, or create cash flow elsewhere to fund the perpetual coupon. All options hurt at least one stakeholder group, according to Mallers. “So the question is, can you come up with a financial engineering strategy where everybody wins?” said Maller.

Mallers Points To Strike Lending Business As Cash Flow Alternative

Mallers said he likes the cash flow path, citing Strike’s Bitcoin-backed loan company, which is pegged at a current addressable market of $20 billion to $30 billion and a long-term possibility of $1 trillion to $2 trillion. He said he did not pursue the permanent preferred model at Twenty One since he did not yet completely grasp it.

Mallers followed up on comments he made at a BTC Prague digital credit panel earlier this month, where he questioned Saylor on the multiple-to-net-asset-value technique and asked for an example of a dilutive transaction within his framework. Saylor responded that MNAV is one of several valuation frameworks and that Strategy's equity issuances become "massively accretive" when liabilities and asset purchases are factored in correctly.

MSTR’s price closed down over 3% on Friday. On Stocktwits, retail sentiment around MSTR remained in the ‘bullish’ zone, while chatter dropped to ‘normal’ from ‘high’ levels over the past day.

XXI’s stock closed down over 2% on Friday. On Stocktwits, retail sentiment around XXI remained in the ‘neutral’ zone, while chatter stayed at ‘low’ levels over the past day.

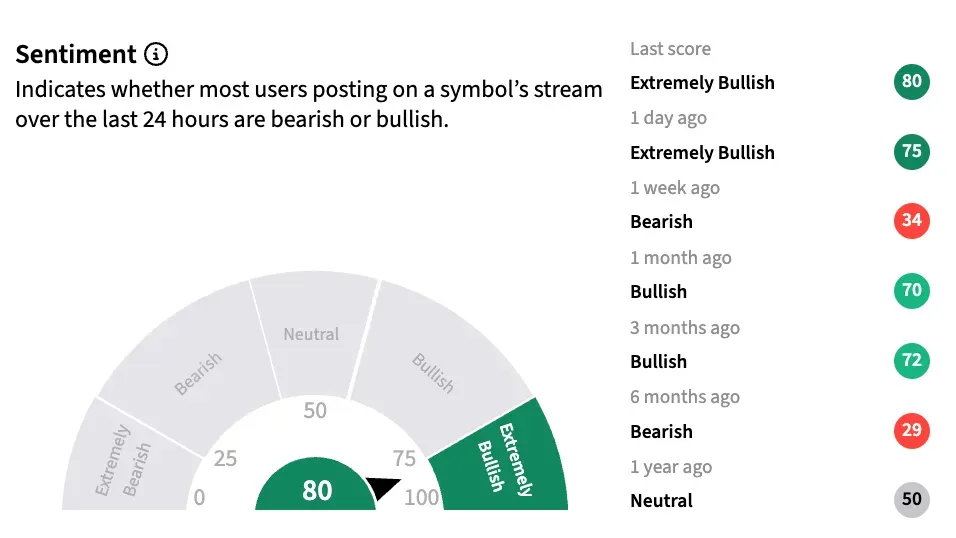

As of Saturday, STRC's price has slid below its $100 issuance par value and was trading at $88, down 10% in a month. On Stocktwits, retail sentiment around STRC remained in the ‘extremely bullish’ zone, while chatter stayed at 'extremely high’ levels over the past day.

Read also: Arthur Hayes Says Michael Saylor Is Pulling 'Jedi Mind Tricks' On Whether Strategy Will Sell More Bitcoin

For updates and corrections, email newsroom[at]stocktwits[dot]com<