Saylor said a well-capitalized Bitcoin treasury company should outperform Bitcoin itself if Bitcoin's annualized rate of return exceeds the company's cost of capital.

- Strategy's Michael Saylor introduced two metrics, BPS and CEBE BPS, to judge whether a Bitcoin treasury company can outperform Bitcoin itself.

- Saylor said the gap between the two, called "Amplification," only appears once a company takes on debt or preferred shares.

- He said short-duration, high-cost liabilities can turn Amplification into underperformance, while long-duration, low-cost liabilities can turn it into upside.

Strategy (MSTR) Executive Chairman Michael Saylor laid out a framework on Sunday for judging whether a Bitcoin (BTC) treasury company can actually beat Bitcoin's own returns, or whether it's quietly falling behind it.

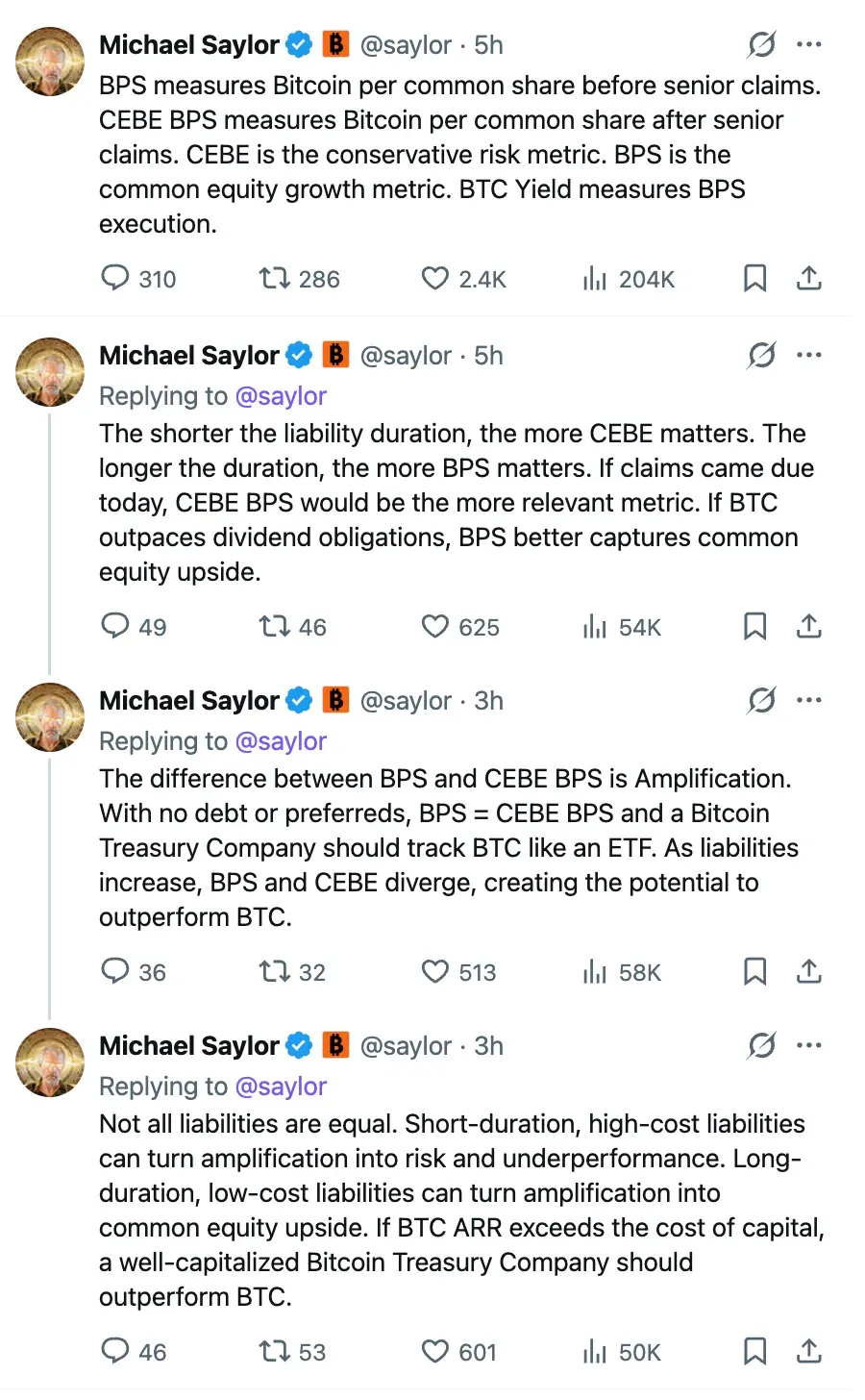

On X, Saylor said the starting point was simple and depended on how much Bitcoin is behind each share of a stock. He called this number BPS, or Bitcoin Per Share.

"BPS measures Bitcoin per common share before senior claims," he wrote, meaning it's calculated before accounting for anything the company owes to debt holders or preferred shareholders. He said that if a company has no debt and no preferred stock, this number tells the whole story, and the stock should move roughly in line with Bitcoin's price, similar to a Bitcoin exchange-traded fund (ETF).

But Saylor pointed out that most Bitcoin treasury companies do carry debt or preferred shares, and for those companies, BPS alone doesn't capture the full picture. So he introduced a second number, CEBE BPS, which he said "measures Bitcoin per common share after senior claims." In other words, CEBE asks what would be left for common shareholders if the company had to pay off everything it owes right now, using its Bitcoin holdings to do so.

Saylor described BPS as the "common equity growth metric" and CEBE as the "conservative risk metric,” one shows the upside, the other shows the floor.

Debt Is A Lever, Not Just A Risk

Saylor said the relationship between these two numbers, BPS and CEBE, is what determines whether a Bitcoin treasury company can actually beat Bitcoin's own returns. "The difference between BPS and CEBE BPS is Amplification," he wrote. "With no debt or preferreds, BPS = CEBE BPS, and a Bitcoin Treasury Company should track BTC like an ETF. As liabilities increase, BPS and CEBE diverge, creating the potential to outperform BTC."

In other words, once a company borrows money to buy more Bitcoin, the gap between the two numbers opens up, and that gap, which Saylor calls “Amplification”, can swing in either direction.

With cheap debt that doesn't need to be repaid for a long time, that borrowed money buys more Bitcoin upfront, and if Bitcoin keeps rising, the extra Bitcoin can boost returns for every shareholder faster than if the company had taken on no debt at all.

But Saylor was careful to note this isn't automatic. "Not all liabilities are equal," he wrote. "Short-duration, high-cost liabilities can turn amplification into risk and underperformance. Long-duration, low-cost liabilities can turn amplification into common equity upside."

The framing echoes comments Saylor made a day earlier, where he argued that whether a capital raise is dilutive or accretive depends on how the funds are used and the company's net assets per share after liabilities.

If a company takes on debt that's expensive or needs to be repaid soon, the same leverage that could have boosted returns instead becomes a liability. The company may be forced to sell Bitcoin or issue new shares to cover those payments, regardless of where Bitcoin's price stands at the time.

Saylor's framework offers a lens for evaluating Strategy's own Stretch (STRC), a preferred stock product that pays holders a high dividend yield. Under his model, STRC is exactly the kind of liability that creates Amplification, and whether that Amplification helps or hurts common shareholders depends on the test Saylor laid out.

Saylor's One-Line Test

Saylor summed up the entire framework with a single benchmark. "If BTC ARR exceeds the cost of capital, a well-capitalized Bitcoin Treasury Company should outperform BTC,” he said. ARR refers to Bitcoin's annualized rate of return, so the test boils down to whether Bitcoin's yearly gains are bigger than what it costs the company to borrow.

If they are, the debt works in the shareholders' favor. If they aren't, that same debt becomes a drag, and the company can underperform Bitcoin even while holding more of it on its balance sheet.

MSTR’s stock was up by 0.33% during after-hours trading. On Stocktwits, the retail sentiment around MSTR remained in the ‘bearish’ zone, while chatter around it stayed at ‘normal’ levels over the past day.

Read also: Iran-US Draft Deal Would Reopen Hormuz, Free $25 Billion, Waive Oil Sanctions: Report

For updates and corrections, email newsroom[at]stocktwits[dot]com<