What used car loan approval really depends on in India: CIBIL, income, documents, down payment, foreclosure, and the rate factors lenders weigh.

A used car loan in India is approved on five things: your credit score, your monthly income stability, the car's age and condition, your down payment, and the lender's appetite for that car. Advertised rates start near 9 to 11% p.a., but the rate you actually receive depends on your profile. Typical tenures are 1 to 6 years, processing fees are 1 to 2% of the loan amount, and foreclosure charges are usually around 5% plus GST. Approval can be same day for clean profiles, but interstate cars or older vehicles add days, not hours.

Why this question is so confusing

Used car finance has no single rate. Each lender prices the loan based on your borrower profile and the car as collateral. So the same buyer can be quoted 10.5% from one lender and 14% from another for the same car. The marketing line on every loan page reads "starting from X%", but that is a floor, not a promise. Before you fill any application, it helps to understand what changes that rate.

Related Articles

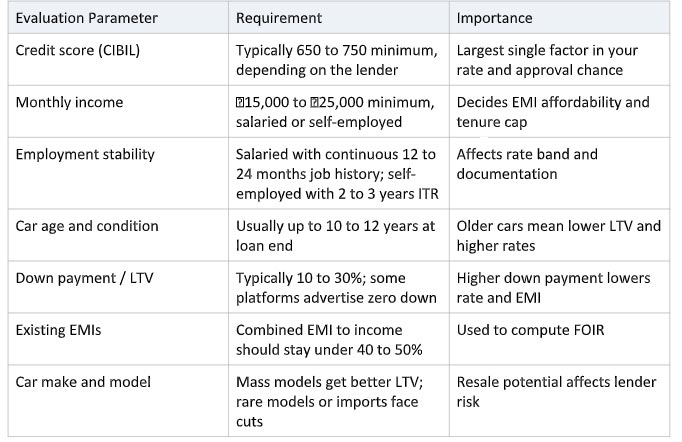

What does the lender actually evaluate?

Most banks and NBFCs run a similar checklist before approving a used car loan. The weights differ, but the inputs are the same.

What documents do you actually need?

Most lenders ask for the same core documents. Have these ready and your approval moves faster.

- Identity proof: PAN card is mandatory; Aadhaar is preferred for KYC

- Address proof: Aadhaar, driving licence, voter ID, passport, or recent utility bill

- Income proof for salaried: last 3 months' salary slips and Form 16 or ITR

- Income proof for self-employed: last 2 to 3 years ITR with computation, plus 6 months bank statement

- 6 months bank statement showing salary credit or business turnover

- Vehicle documents: RC, insurance, valuation report or inspection certificate

- Two passport-size photographs

- Cancelled cheque for the ECS or NACH mandate

What are realistic rates and tenures right now?

Used car loan rates in India typically range from about 8.9 to 16% p.a., depending on lender, profile, and tenure. Banks usually price salaried borrowers with a strong CIBIL score in the lower half, and NBFCs price slightly higher but cover thinner profiles. Tenures stretch up to 6 years. Beyond 5 years, the total interest paid often exceeds the savings from a lower EMI.

What slows down approval?

- CIBIL below 650 or recent late payments on any existing loan

- Multiple credit enquiries in the last 30 days from different lenders

- Salary credited in cash or through unstable channels

- Mismatch between PAN, Aadhaar and bank account name

- Car older than 10 years or with unclear ownership trail

- Pending challans or hypothecation issues on the RC

- Inter-state purchase that needs NOC and re-registration before disbursal

How does platform-assisted finance differ from bank finance?

Organised used car platforms aggregate multiple lenders behind one application. You give documents once. The platform routes the file to two or three lenders and shares offers. The trade-off is speed against negotiation. You get one consolidated offer fast, but you might leave a few points of rate or fee on the table compared to walking into your own bank where you already have a relationship.

As an example, Cars24 provides loan tenures up to 6 years, in-house and partner lender options, and same-day disbursal for eligible profiles. Whether "same-day" applies to your file depends on documentation, the car, and the lender chosen.

What about foreclosure and early closure?

Foreclosure is the most ignored part of a used car loan, and the most painful one if you do not plan for it. Most lenders charge around 5% plus GST on the outstanding principal if you close the loan early. That cost matters in two cases: when you want to return a financed car during the 30-day return window, and when you plan to sell or refinance within the first year. Ask for foreclosure charges in writing before signing.