The fuel surcharge waiver is one of the most direct and predictable credit card benefits, helping cardholders save on every qualifying fuel transaction.

Fuel credit cards let you earn rewards or cashback on your daily fuel expenses. With fuel prices remaining high and fuel costs taking up a larger share of many household budgets, evaluating these benefits has become more relevant than ever. However, the actual savings depend on several factors that many cardholders do not examine closely. Understanding these details can help you choose a card that genuinely reduces fuel costs instead of offering minimal value.

How fuel credit card rewards are structured

Fuel credit cards usually offer savings through one or more of the following:

Related Articles

- Cashback on fuel transactions as a percentage of the amount spent.

- Reward points are redeemable against fuel bills or statement credit.

- Surcharge waivers on fuel transactions, which ordinarily attract a levy of 1% to 1.5% of the transaction value.

- Accelerated reward rates at partner fuel station networks.

The fuel surcharge waiver is one of the most direct and predictable credit card benefits, helping cardholders save on every qualifying fuel transaction. When paired with accelerated rewards on fuel spends, the savings can become even more meaningful for those who refuel regularly. The IDFC FIRST Bank FIRST Power+ Credit Card combines both benefits, allowing cardholders to earn rewards while reducing a portion of their fuel-related costs. For frequent drivers and daily commuters, this can help make rising fuel expenses a little easier to manage.

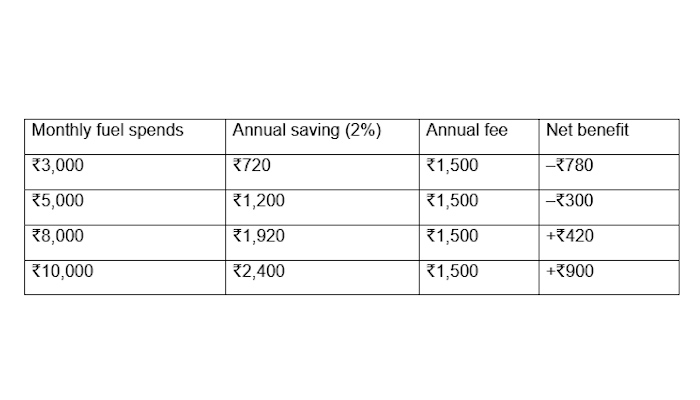

Breaking down the numbers: fees vs actual savings

Whether a fuel card saves money comes down to two figures: what the card earns back through cashback and surcharge waivers, and what it costs to hold in annual fees. The table below uses a 2% combined saving rate (1% cashback + 1% surcharge waiver) against a ₹1,500 annual fee to show how the net outcome shifts with spend:

Calculation mentioned in the table are generic and can vary depending on the card you choose and your spending pattern.

The table makes the pattern clear: at lower spend levels, the annual fee outweighs the benefit; the card only starts working in the cardholder's favour as monthly usage climbs.

When do you actually save?

Fuel credit cards generate a net positive outcome under specific conditions:

- Monthly fuel spend exceeds a certain spend threshold.

- Transactions are conducted at eligible fuel stations within the card's partner network.

- The surcharge waiver applies to the card's transaction tier.

- The card carries no annual fee, or the fee is waived upon meeting a minimum annual spend.

Many card issuers set a minimum and maximum transaction amount for surcharge waiver eligibility. Transactions below ₹400 or above ₹4,000 may usually not qualify, depending on the bank’s and the card's terms. Cardholders who apply for a credit card online should verify these terms in the card's schedule of charges from the bank’s website before applying, rather than relying solely on headline marketing figures.

When are the savings overstated?

Several factors reduce the effective value of a fuel card below its advertised rate:

- Reward expiry: Points accumulated on fuel spend often carry an expiry of 12 to 24 months; unredeemed points produce no financial benefit.

- Transaction caps: A monthly cap on qualifying fuel spend means the reward rate drops to zero beyond that cap.

- Category exclusions: Certain fuel station types, including those operated by small independent dealers, may be excluded from the reward category.

- Redemption friction: Some cards restrict point redemption to specific portals; if the process is inconvenient, accumulated points may go unused.

These terms are not always disclosed upfront, which is why reading the full schedule of charges before selecting a card matters more than reviewing the summary offer page.

Reward points and cashback are also not equivalent in value. A card offering 10 points per ₹100, where one point equals ₹0.10, delivers ₹1 in effective value, which is the same as a card offering a flat 1% cashback. The rupee equivalent shifts materially by redemption category.

Maximising savings on fuel and road travel with IDFC FIRST Bank credit cards

For individuals who frequently spend on fuel and highway travel, the IDFC FIRST Bank Power and Power+ Credit Cards offer benefits that can help offset everyday expenses.

IDFC FIRST Power+ credit card

- Save up to ₹18,500 annually

- Up to 6.5% savings on fuel expenses

- 5% savings as rewards on IDFC FIRST FASTag recharges

- Welcome benefits worth ₹2,500

- Annual fee: ₹499 + GST

- Annual fee waived on spends of ₹1.5 lakh or more in a year

IDFC FIRST Power credit card

- Save up to ₹7,000 annually

- Up to 5% savings on fuel expenses

- 2.5% savings as rewards on IDFC FIRST FASTag recharges

- Welcome benefits worth ₹2,250

- Annual fee: ₹199 + GST

- Annual fee waived on spends of ₹50,000 or more in a year

- Finding the right card for your fuel expenses

Before selecting a fuel credit card, cardholders should compare the effective cashback equivalent of reward points rather than point counts, verify break-even spend against their actual monthly usage, and check which station networks qualify. Cardholders who want to start the credit card apply online process can use published benefit schedules from issuers, including IDFC FIRST Bank, to run this comparison independently rather than relying on summary offer pages.