While PepsiCo faces slowing North American demand, international growth remains a key source of optimism.

- Barclays lowered its price target on PepsiCo to $144 from $158 and kept its Equal Weight rating.

- The firm cited concerns that the North American foods turnaround is losing momentum.

- Last week, JPMorgan cut its price target on PepsiCo to $170 from $178, citing weaker pricing, product mix and soft demand trends.

PepsiCo (PEP) stock is facing caution from Wall Street after Barclays lowered its price target on the beverage and snacks giant ahead of its second-quarter earnings, reflecting growing concerns about the pace of recovery in the company’s North American food business.

Barclays Sees PEP’s Turnaround Losing Momentum

Barclays cut its price target on PepsiCo shares to $144 from $158 while maintaining an ‘Equal Weight’ rating, citing concerns that improvements seen earlier this year may be difficult to maintain.

Analysts at Barclays said PepsiCo has lagged behind many of its consumer staples peers as investors question whether the company's turnaround strategy for its North American foods segment can deliver lasting results.

According to the firm, ongoing weakness in the company's core unflavored snack portfolio continues to limit the potential for a stronger recovery.

In addition to trimming its price target, Barclays reduced its sales projections for PepsiCo ahead of the Q2 earnings. The firm believes the company's operational improvements have not advanced enough to fully offset continued challenges in key product categories.

PepsiCo stock edged 0.08% lower overnight, ahead of Monday.

UBS also lowered its price target on PepsiCo to $172 from $186.

JPMorgan Predicts Soft Demand For PepsiCo

Last week, JPMorgan reduced its price target on PepsiCo to $170 from $178 but maintained an ‘Overweight’ rating, reflecting continued confidence in the company's longer-term outlook despite softer near-term expectations.

The firm lowered its Q2 forecasts, expecting weaker pricing, a less favorable product mix and slower revenue growth than previously expected. JPMorgan also said recent sales data points to soft demand, leading to a more cautious outlook for the quarter.

According to Koyfin data, analysts expect PepsiCo to report Q2 revenue of $23.9 billion and earnings of $2.21 per share.

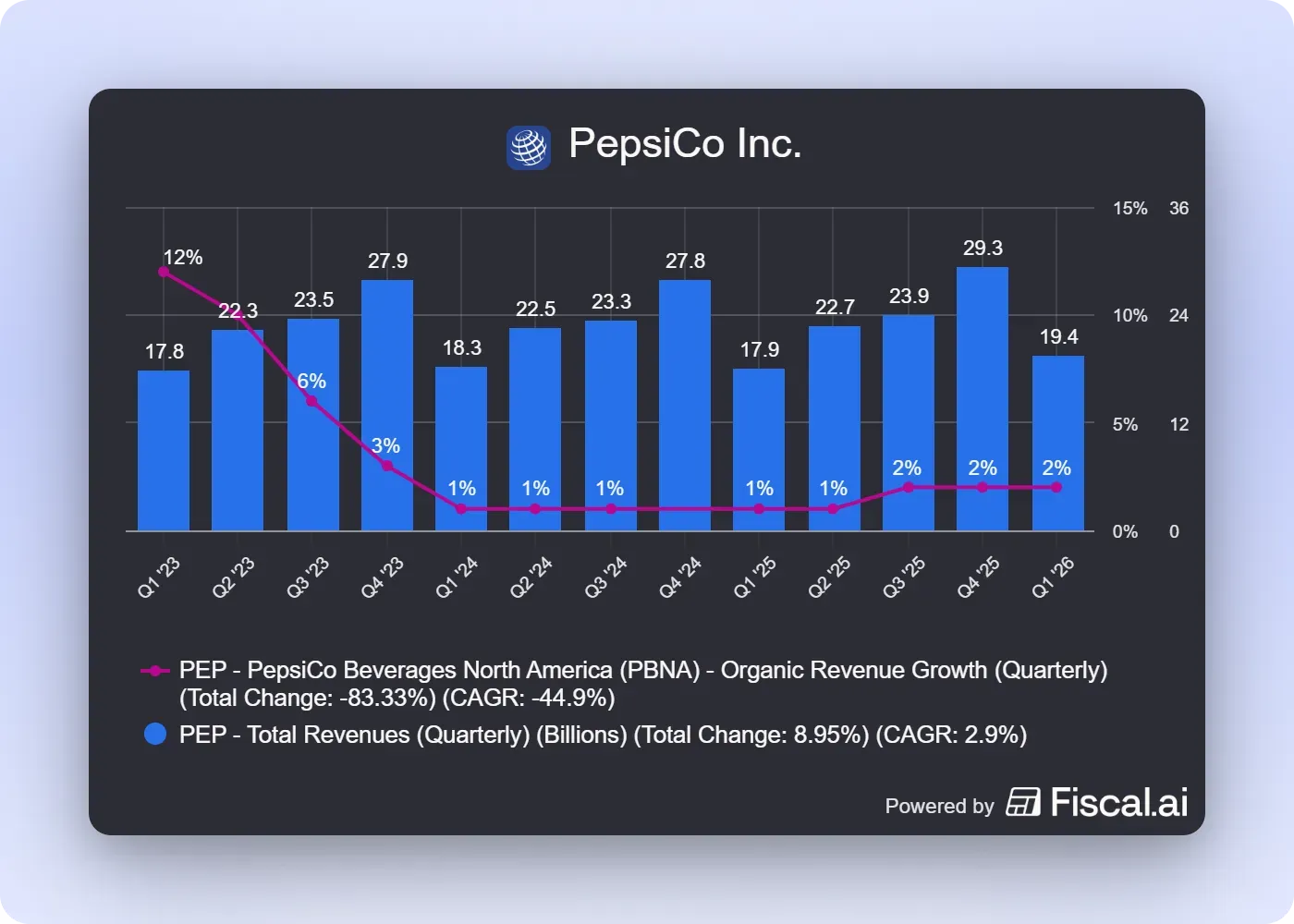

PepsiCo has been relying heavily on price increases to offset inflation over the past two years. So the Q2 results are expected to offer insight into changing consumer spending patterns and the effectiveness of its evolving business strategy.

While PepsiCo's North American food division continues to face slower demand, investors expect stronger growth from overseas operations to provide support. Latin America and the Europe, Middle East and Africa regions are projected to outperform the company's domestic business.

On Stocktwits, retail sentiment around the stock turned to ‘neutral’ from ' bullish’ territory the previous day with a 400% increase in message volume over the last 24 hours.

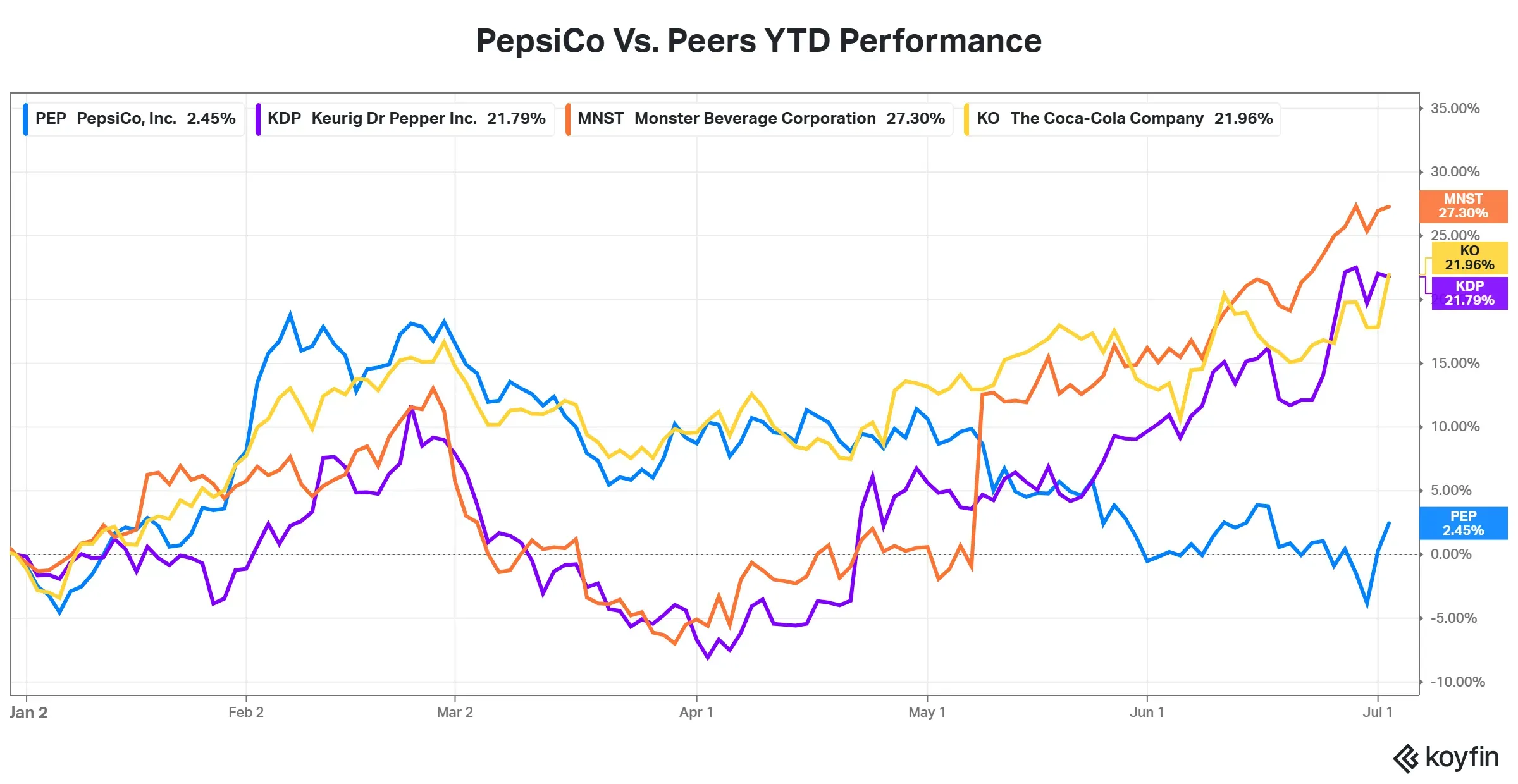

PEP stock has gained 0.5% year-to-date.

For updates and corrections, email newsroom[at]stocktwits[dot]com.<