With the crypto user base being about 75% of the way to reaching one billion, some crypto companies like Binance are preparing for the inevitable need for more compliance bandwidth.

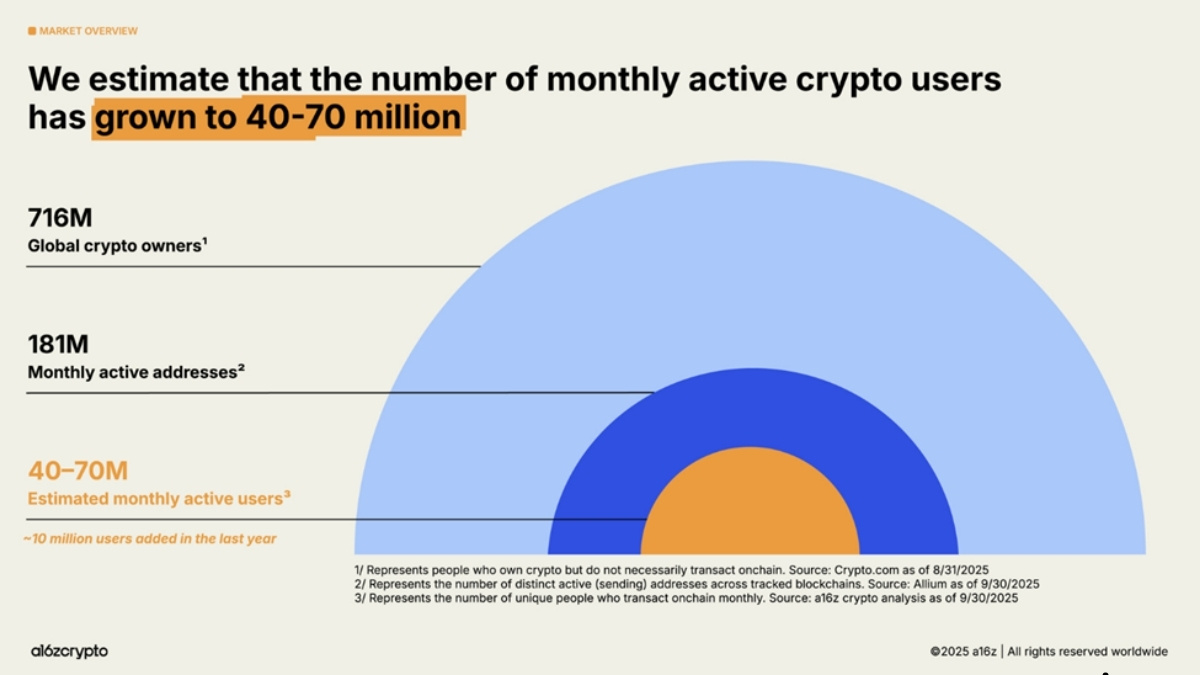

According to recent industry estimates, the total number of crypto users worldwide was estimated to be around 716 million at the end of 2025, representing a significant increase over the previous year. While this news is encouraging for those hoping for more growth in the sector, growth also comes with growing pains. As the crypto space edges ever closer to one billion users, crypto companies will need to come to terms with what serving such a large audience, while also maintaining the necessary compliance infrastructure, will entail.

Rules are tightening across the globe and bad actors and sanctions evaders are on the rise. Will big crypto players be able to keep up?

The Cost of Compliance Efforts

Related Articles

Building financial compliance infrastructure is no longer an optional add-on. Instead, it has become an essential cost center for every major company that handles cryptocurrency. The cryptocurrency exchange Binance recently published a blog post outlining this cost, writing, “Binance invests hundreds of millions of U.S. dollars in its compliance program, and a significant share of these resources is dedicated to maintaining a world-class compliance team.” The post also notes that the company currently employs around 1,500 people that work entirely on compliance and related issues.

This may seem to the untrained eye to be excessive, but the costs of failing to comply or allowing bad actors to take advantage of an exchange can be dire. In January of 2025, BitMEX faced a $100 million fine for “failing to establish, implement, and maintain an adequate anti-money laundering (“AML”) and know-your-customer (“KYC”) program.” In Canada, the exchange Cryptomus is facing a $176 million fine from FINTRAC for allegedly failing “to comply with a Ministerial Directive, as demonstrated in connection to financial transactions associated with the Islamic Republic of Iran,” amongst other possible violations. Compliance violations aren’t just costly, but they can also damage a company's reputation. That’s why exchanges are stepping up to be proactive instead of just reactive.

Scaling Compliance Infrastructure

With the crypto user base being about 75% of the way to reaching one billion, some crypto companies like Binance are preparing for the inevitable need for more compliance bandwidth. That continued investment in compliance was challenged recently amid media allegations of sanctioned funds flowing through the exchange.

In a recent interview on The David Lin Report, Binance Chief Compliance Officer Noah Perlman discussed the allegations, “This is very personal to me. We’ve spent the last three years since I’ve been here really dedicated full energy to building a great program and improving everything. And when we have false accusations like this it really strikes not just at me but at all the men and women here that are working to really improve compliance.” Perlman continued, “The idea that we would dismiss employees for raising something — it’s just actually preposterous on its face, as evidenced by the fact that the investigation continued, the relevant accounts were offboarded and relevant reporting was made.”

A federal judge dismissed the civil lawsuit against Binance on Friday, March 6th. Binance's General Counsel Eleanor Hughes commented on the dismissal, “This dismissal is a complete vindication of all false allegations. The court has unambiguously rejected the false and damaging narrative that Binance assisted terrorists. We have always maintained that these claims were without merit, and today's ruling confirms that. We will continue to defend ourselves aggressively against any litigation or reporting that misrepresents who we are and how we operate."

While some users may actively try to use crypto as a means to launder money around the world, exchanges like Binance continue to focus on regulatory compliance and security. One of the latest examples of this focus was the recent headline announcement of Binance being the first crypto exchange to acquire a global license under the ADGM framework. The license is granted by the FSRA body of Abu Dhabi in the UAE. The certification, according to the company, will give Binance “a new level of credibility and seamless access across multiple markets, extending well beyond the UAE, thus cementing our position at the forefront of regulatory progress in digital finance.”

Abu Dhabi has become an emerging hub of crypto and financial development. According to global law firm DLA Piper, when the Emirate “became the first jurisdiction globally to introduce and implement a comprehensive and bespoke regulatory framework for the regulation of exchanges, custodians, brokers, and other intermediaries engaged in VA activities.”

Navigating the Evolving Regulatory Landscape

The outlook for big crypto players in the future is complex and shifting. Many countries treat crypto like a gray area with vague laws and uneven enforcement. That will inevitably change as crypto dominance increases and more countries develop better frameworks for compliance teams to follow.

But as more people enter the crypto space, more bad actors will inevitably follow. This means that regardless of how laws solidify or shift, crypto companies will need to continue to develop their own compliance teams and technologies in order to stay ahead of the coming challenges.