Tesla’s Core EV Business Is Feeling The Heat — What Its Automotive Segment Really Delivered In 2025

Synopsis

Tesla’s stock strength is decoupling from auto fundamentals, with the outperformance now hinging on robotaxis and AI optimism despite a maturing, slowing EV business.

- Deliveries are poised to fall for a second straight year and 2026 growth expectations diverge sharply between Wall Street and more cautious investors.

- The investment debate hinges on non-auto upside, with bulls betting on FSD, robotaxis, and Optimus.

- But skeptics argue that weak auto performance limits funding and upside for these initiatives.

Tesla, Inc.’s (TSLA) stock is on track to outperform the consumer discretionary sector this year, helped in part by the robotaxi chatter that picked up pace in the last few months of the year, even as the flagship electric vehicle (EV) business sagged.

Negative headlines surrounding Tesla’s EV business continue to emerge. Earlier this week, Bloomberg reported that Tesla’s contract value with South Korean supplier L&F Co. has been slashed by 99%.

Maturing Automotive Business?

Automotive deliveries growth hasn’t really picked up after the spurt seen in the aftermath of the COVID-19 pandemic. After peaking at 83% in the second quarter of 2023, year-over-year sales growth either slowed or turned negative. The third quarter of 2025 marked a recovery after two consecutive quarters of decline; however, the 7.4% growth rate remained well below the nearly 122% surge recorded in the second quarter of 2021, when Model Y sales soared following its 2020 launch.

Tesla for the first time publicly shared the consensus delivery forecast for the fourth quarter, ahead of the formal release scheduled for Jan. 2. The company-compiled consensus analyst forecast for the quarter is 422,850. If the estimate proves accurate, the company is on track to report annual deliveries of 1.641 million, down 8.3% from 1.79 million in 2024. Incidentally, it would also mark the second straight year of sales decline.

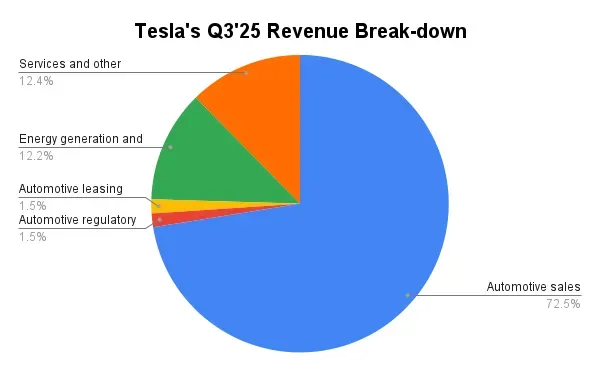

The automotive segment, which includes vehicle sales, regulatory credits, and leasing revenue, still accounts for a lion’s share of Tesla's revenue.

Chart generated using company data<

The outlook isn’t very optimistic either. While the consensus view shared by Tesla shows that the company might return to growth in 2026, which, though, is likely to be anemic (6.7%), Deepwater Asset Management’s Gene Munster predicts a big miss. In his 2026 predictions, the fund manager said he expects 2026 sales to be flat to up 5% as opposed to Wall Street’s consensus forecast for 16% delivery growth.

If the auto business continues to be weak, one of the worst hit could be Musk himself. His $1 trillion pay package, which the Delaware Supreme Court recently cleared, is predicated on the company’s market cap hitting $8.5 trillion, while also meeting the following operational performance:

-achieving up to $400 billion in earnings before interest, taxes, depreciation and amortization (EBITDA)

-delivering 20 million cars cumulatively

-selling 1 million robots

-selling 10 million FSD subscriptions

- operating 1 million robotaxis

Non-Autos To Drive Investment Case?

Munster, though downbeat on the core auto business, says his investment case doesn’t change, and it is still predicated on full self-driving software, robotaxis, and Optimusm humanoid robots. He also opined that robotaxis without a safety driver will likely get regulatory clearance by the end of the year.

Morgan Stanley’s Andrew Percoco, who downgraded Tesla to ‘Equal-Weight’ from ‘Overweight’ earlier this month, sees a challenging catalyst path over the next 12 months, presenting downside risk to consensus estimates. At the same time, the analyst believes the positive catalysts for its non-auto business are already reflected in the stock price. Emphasizing the importance of the auto business, the analyst said:

“While it is well understood that Tesla is more than an auto manufacturer, we believe it will be increasingly challenging to support meaningful upside to Tesla shares barring an improvement, or at least stabilization, within its auto business, which is a key source of funding for its non-auto businesses.”

Tesla bull Daniel Ives, however, sees 2026 as a “monster year” for Tesla as the autonomous and robotics chapter begins.

“We expect in early 2026 an easing of the federal framework for autonomous vehicles, with more power going to the federal regulators, with states having less authority on the autonomous rules framework likely under an Executive Order.”

The analyst expects Tesla to reach a $2 trillion market capitalization by 2026, with a bull-case scenario pointing to as much as $3 trillion by year-end.

What Retail Traders & Analysts Feel About TSLA

Retail sentiment toward the Tesla stock was ‘bearish’ as of early Tuesday, tempering from the bullish mood seen three months ago, when it began gathering some momentum.

According to Koyfin, the average analyst price target for Tesla’s stock is $399.15, implying more than 13% downside from current levels. Of the 46 analysts covering the stock, 19 have buy-equivalent ratings, 16 remain on the sidelines and a sizeable number of 10 analysts rate it as a ‘Sell.’

For updates and corrections, email newsroom[at]stocktwits[dot]com.<

Stay updated with all the latest Business News, including market trends, Share Market News, stock updates, taxation, IPOs, banking, finance, real estate, savings, and investments. Track daily Gold Price changes, updates on DA Hike, and the latest developments on the 8th Pay Commission. Get in-depth analysis, expert opinions, and real-time updates to make informed financial decisions. Download the Asianet News Official App from the Android Play Store and iPhone App Store to stay ahead in business.