BYD, Haidilao Or PDD: ‘Big Short’ Investor Michael Burry Says He's Buying One Of These Chinese Stocks As Earnings Loom

Synopsis

Burry prefers Haidilao over BYD and PDD due to its strong cash generation, dividend payouts and growth potential as China’s only national hot-pot chain.

- Michael Burry said Chinese stocks have suffered “1929-style crashes while the businesses kept growing.”

- He said a reversal in sentiment could unlock “significant upside potential” for Hong Kong-listed companies.

- Haidilao was Burry’s top pick, with the hot-pot chain generating about $870 million in free cash flow in 2024.

Michael Burry, the investor famous for predicting the U.S. housing crash and profiled in Michael Lewis’ book “The Big Short,” said he currently favors one Chinese stock among BYD, Haidilao and PDD as investors brace for their earnings reports expected later this month.

PDD is set to report earnings on March 19, BYD on March 23, and Haidilao on March 31.

In a blog post on Hong Kong-listed companies, Burry said that Chinese equities “have had 1929-style crashes while the businesses kept growing. This has never happened in market history going back to 1900.”

Burry Sees Rebound In Hong Kong Stocks

Burry attributed the plunge in Chinese equities to regulatory shocks, macro turmoil, and battered investor sentiment, rather than failing fundamentals. He cited Beijing's crackdown on tech firms, the 2021 global asset bubble burst, China's property market collapse, and COVID-19 pandemic lockdowns as the key culprits. But when sentiment turns, he argued, it could converge with rising earnings to create "significant upside potential" in Hong Kong-listed shares.

Burry Calls BYD A ‘Mild Buy’

Bury called EV giant BYD one of the world’s most technologically advanced automakers because of its vertically integrated model: the company manufactures its own chips, batteries, motors and other components. A key advantage is BYD’s Blade battery, which uses lithium iron phosphate, Burry said. He added that the design is cheaper and safer than the nickel-manganese-cobalt batteries widely used by rivals like Tesla.

Burry said that BYD also benefits from a large working-capital windfall after pivoting away from selling primarily to Chinese government buyers. When government receivables were finally collected, the shift released about 40 billion yuan ($5.8 billion) in cash that helped fund overseas factory expansion.

Burry rated the stock 7 out of 10, calling it a “mild buy” and said he would be an “aggressive buyer at HK$75 or better, if the thesis still holds at that time.”

Burry Sees Hot Potential In Haidilao

Burry suggested that Haidilao International, China’s only national hot pot restaurant brand, currently offers the most compelling opportunity. It still holds just about 2.2% of the market, he said, leaving significant room for expansion. Burry rated the stock 8 out of 10.

He said Haidilao’s dining concept often feels like “mixing a luxury hotel with a hot pot restaurant,” but added it made a costly mistake by rapidly expanding during the COVID-19 pandemic, opening 540 restaurants between 2020 and 2021 just before China imposed strict lockdowns. The company later closed about 300 locations after the expansion and wrote off roughly two-thirds of the spending.

Despite the setback, Haidilao generated about $870 million in free cash flow in 2024 and paid out 94% of earnings as dividends. Burry also said the food-delivery subsidy war among Meituan, Alibaba Group and JD.com inadvertently benefited restaurant chains as they spent roughly 100 billion yuan ($14 billion) on delivery incentives. “At the delivery companies’ expense, Haidilao acquired many new customers,” he said.

Burry Calls PDD Disclosure Problems ‘Vexing’

Burry was more cautious about PDD Holdings, the parent company of Pinduoduo and Temu. He noted that the company built a profitable model in part by delaying payments to merchants while collecting customer payments for extended periods. “PDD would receive the order, arrange the drop ship, and then not pay its farmer suppliers for 500-600 days,” Burry said.

The float once generated enough investment income to account for nearly all of the company’s profits. However, the model has faced growing challenges. Temu’s growth slowed after the U.S. closed a shipping loophole that allowed tariff-free imports, while competition intensified in China from JD.com and Alibaba.

Meanwhile, Burry also raised concerns about the company’s financial disclosures. “PDD’s problem with disclosure is vexing,” he said, noting that the company provides little detail about revenue by geography, product, or business line.

A short-seller report in 2018 alleged accounting discrepancies, though Burry said he believes the report likely overlooked part of the company’s complex structure. “Overall, I cannot call it fraud. I can call it bad disclosure, the worst,” he said.

Burry rated PDD 6 out of 10, saying the stock could not justify a full position because of disclosure concerns. “I would keep it around 2%, roughly one-third of my typical full position, until disclosure is satisfying to me,” he said.

"By tackling BYD, then Haidilao, and now PDD, I proceeded from best disclosure to disclosure of significant related party dealings and now to very poor disclosure. The middle one is my current favorite of the three for many reasons," Burry said. "One of those reasons is that hiding white collar shenanigans is worse than allowing investors to consider said shenanigans within the context of the total analysis."

How Did Stocktwits Users React?

On Stocktwits, retail sentiment toward PDD was ‘bullish’ while sentiment toward BYD was ‘bearish,’ both amid ‘high’ message volume.

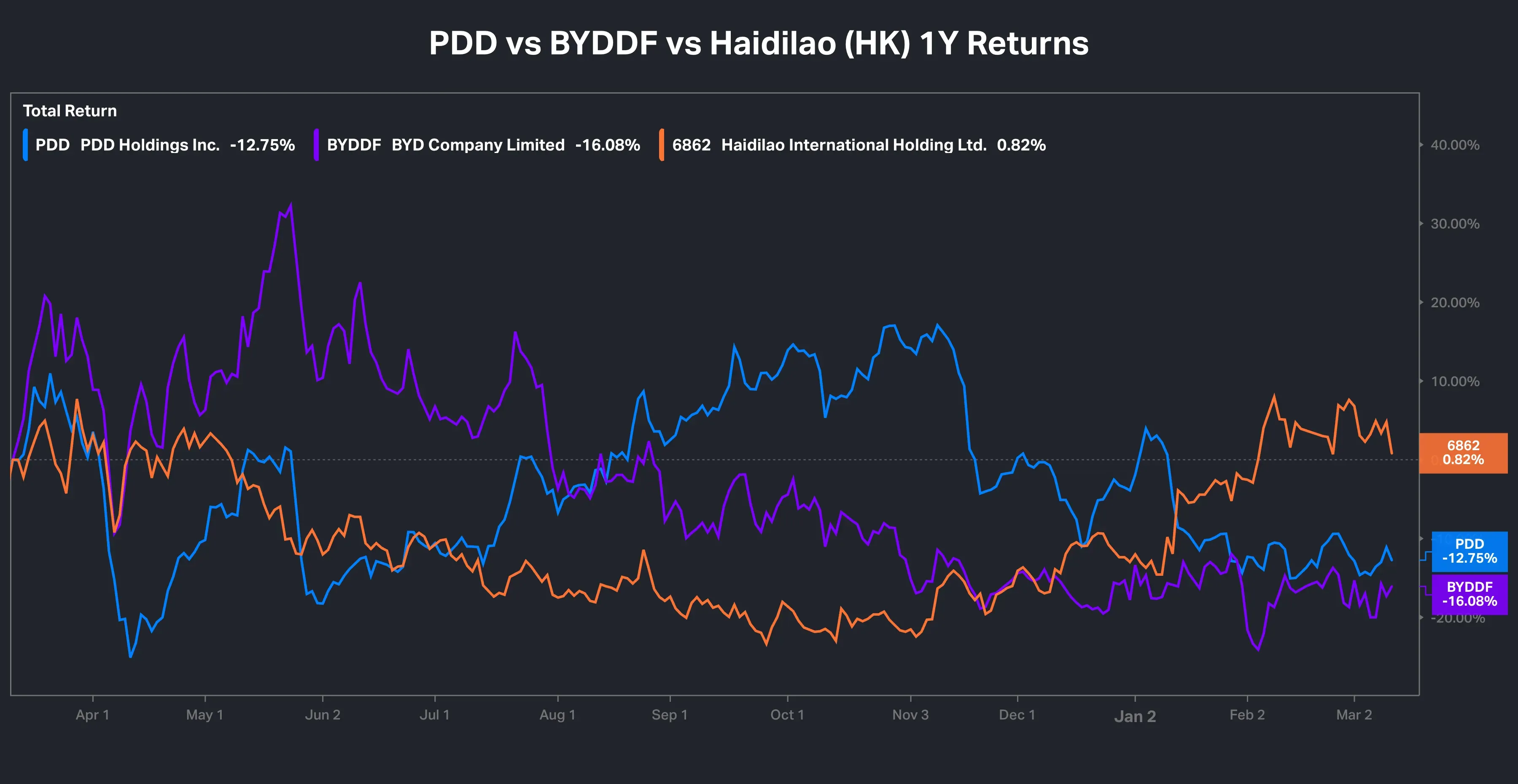

Over the past year, the U.S.-listed shares of BYD and PDD have dropped about 16% and 13%, respectively, while Haidilao is not U.S.-listed.

For updates and corrections, email newsroom[at]stocktwits[dot]com.<

Stay updated with all the latest Business News, including market trends, Share Market News, stock updates, taxation, IPOs, banking, finance, real estate, savings, and investments. Track daily Gold Price changes, updates on DA Hike, and the latest developments on the 8th Pay Commission. Get in-depth analysis, expert opinions, and real-time updates to make informed financial decisions. Download the Asianet News Official App from the Android Play Store and iPhone App Store to stay ahead in business.